There has been much debate on the premium a new private residential property has over a resale property, and how that drives homebuying behaviour. Many questions have been asked about the discount a 99-year leasehold property has over a comparable freehold or 999-year project (herein collectively referred to as freehold).

In this analysis, we look at the data on how prices have moved over time, to see how recent trends may play out.

Over the past decade, whether it is in the prime Core Central Region, the city fringe Rest of Central Region, or the suburban Outside of Central Region, the premium that a new launch commands has increased over resale prices.

A major part of the increase has been due to rising land and construction costs. Between 2013 and 2017, government land sale (GLS) tender prices (adjusted for location and other factors) fell. Thus when the projects were marketed in 2014 and 2018 respectively, developers had the flexibility to rein in on selling prices.

However, in the period 2021 to 2022, not only did land prices accelerate, Covid-led disruptions also caused construction costs to rise sharply and developers had no choice but to raise selling prices of new launches to a new tableau. This widened the gap between new launches and resale properties.

In 2022, when the new batch of post-S$2,000 per square foot RCR and OCR condominiums were released for sale, the premium for new sale leasehold units spiked.

A NEWSLETTER FOR YOU

Tuesday, 12 pm

Property Insights

Get an exclusive analysis of real estate and property news in Singapore and beyond.

However, that gap appears to have hit a ceiling, and the premium has come off, stabilising at around the 10-year historical average.

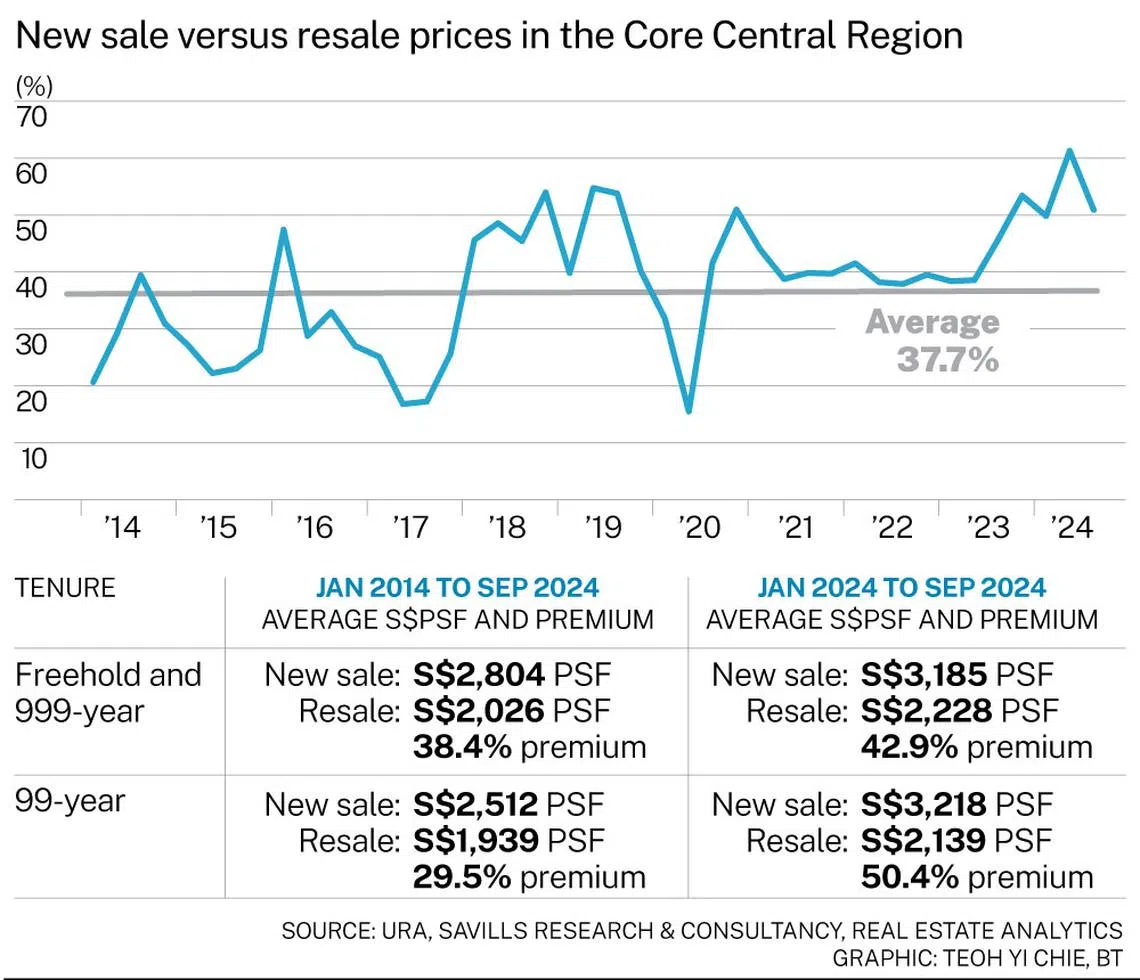

In the prime Core Central Region (CCR), the overall premium for new sale to resale has been widening since mid-2023. Over the period Q1 2014 to Q3 2024, the gap reached a peak of 61.3 per cent in Q2 2024 and last settled at 50.9 per cent in Q3 2024. This is significantly higher than the 37.7 per cent average recorded over the period.

When we turn more granular, we see that it has been units sold in the new sale leasehold market that have pulled up the premium, with the average for the first three quarters of 2024 at 50.4 per cent. The average from the start of 2014 till Q3 2024 had been 29.5 per cent.

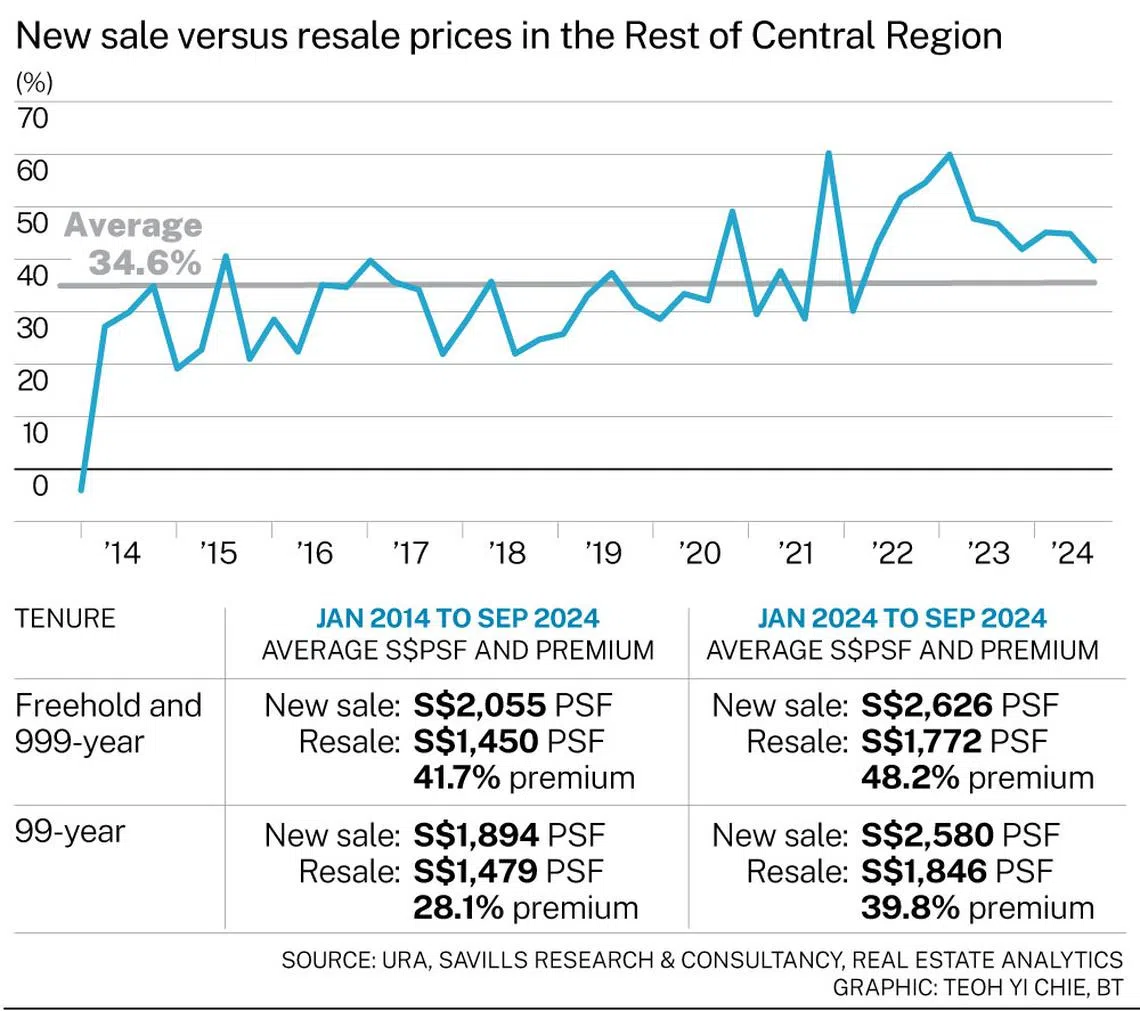

In city fringe locations in the Rest of Central Region (RCR), the overall premium to the average from 2014 to Q3 2024 is much lower than for the CCR.

As at Q3 2024, the premium stood at 39.7 per cent, relatively close to the average of 34.6 per cent. Nevertheless, the premium is still large, and the leasehold new sale market contributed more to building up the premium.

For the first three quarters of 2024, the premium for freehold new to resale was 48.2 per cent versus the long-term average of 41.7 per cent, while the statistic for leasehold was 39.8 per cent with the long-term average at 28.1 per cent.

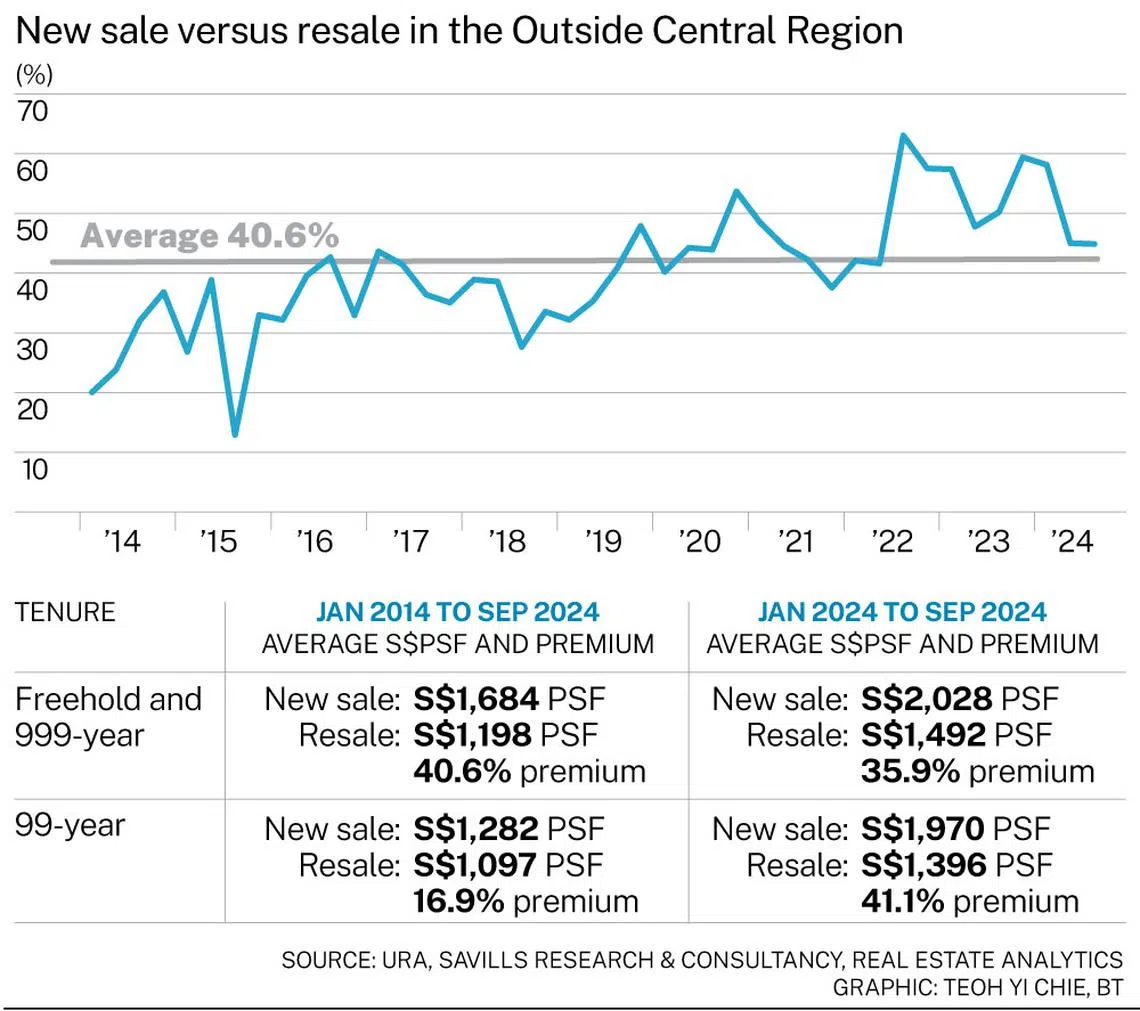

In the OCR suburbs, the premium in Q3 2024 was 44.9 per cent, higher than that in the RCR which registered 39.7 per cent, but below the 50.9 per cent in the CCR. However, similar to what transpired in the RCR, the premium has been trending down in 2024 after peaking at 63.1 per cent in Q3 2022.

The new sale premium for OCR leasehold non-landed properties was 41.1 per cent for the first three quarters of this year, higher than that for freehold.

Additionally, the premium this year has been substantially higher than the 16.9 per cent recorded for the period from 2014 to Q3 2024.

Across all regions, whether a non-landed property is in the CCR, RCR and OCR, the long term trendline has been for premiums to be increasing.

In time, the slope of this trend may flatten. An ageing population would soon create resistance on the rise of private prices purely based on population increasing, leaving rising HDB resale prices as the key driver that creates demand from upgraders.

Unfortunately, upgrading demand is hard to measure because it is difficult to find statistics to ferret out who are the likely candidates that have the means to upgrade.

Thus, one only has hand-wavy explanations to describe or predict why.

For instance, the recent launch Norwood Grand did exceptionally well on the first week of sales, being the first launch in the Woodlands area in 12 years, with a relatively small number of units.

Facing a recent spike up in HDB resale prices in a location where prices have been subdued, potential upgraders there who had used a relatively low amount of their CPF for housing, by now, will have surpluses to upgrade.

Price versus size

Among freehold/999-year new projects, the size of units transacted has been increasing. The median size transacted for this category is in part dependent on the location where collective sales were concentrated a year or two before the launch.

As most freehold/999-year sites are located either in the CCR and part of the RCR, developers these days often design them to cater to the ultra-high net worth or families seeking to upgrade.

For 99-year new sales, unit sizes have generally been quite constant. This is because most of them are derived from Government Land Sales and hence have common parameters that ultimately govern their average sizes.

It is in the resale market that the househunters have been buying smaller units over the past 10 years.

One reason is that rising prices on a S$ psf basis have motivated buyers to accept smaller floor areas to suit their budget.

Another reason is that projects that were first launched a decade ago that had smaller-sized units, are now being released as resale units.

For example, a 99-year new launch in 2014 may have median sizes of about 764 sq ft. These could come to the resale market in the coming years and when co-mingled with projects built before then, the median sizes for resale properties fell.

Buy new or resale?

The answer is not surprising. It depends on the objective of the buyer.

A buyer who intends to move into a private property or reap almost immediate rental income should obviously consider resale properties.

For those who intend to put their savings to good use, such as buying high-yielding instruments, or businesspeople who wish to use dormant cash for working capital purposes, a new sale, notwithstanding its higher premium to resale, may be more optimal.

The progressive payment structure permits them time to recycle their equity in their business before the call for the next progressive payment. Also, for those buying for investment, the rent for a new apartment or condominium is often higher than what older properties can fetch.

Freehold or leasehold?

On whether freehold/999-year or 99-year is a better deal, those buying for investment need to do the sums to calculate the overall return yield.

They would have to factor in the rental yield and the potential of reaping a premium from a collective sale.

For end-users, it doesn’t really matter that much because a freehold/999-year property would have a pricing premium over 99-years to account for the tenure.

It boils down to whether the end-user has an emotional attachment to the property, or if a freehold/999-year lease gives him/her peace of mind.

For those who intend to live in private non-landed properties, the jump in median size transacted for 99-year new sale leasehold is worth commenting on.

This increase could have been borne out of the recent rise in HDB resale prices. From the end of 2020 till Q3 2024, HDB resale prices have risen by 39.5 per cent. In contrast, median new sale prices of non-landed properties in the RCR and OCR rose by 28.3 per cent and 29.2 per cent.

This narrowing in prices between the public and private domains of the market is the likely factor that is motivating HDB upgraders to buy into new sale properties for living in.

For the first three quarters of 2024, HDB resale prices had already risen 6.8 per cent.

In contrast, RCR median prices rose by just 3.6 per cent while those in the OCR fell by 7.2 per cent.

This asymmetrical rate of price changes is likely to spawn greater upgrader demand from the HDB market for larger private homes in the coming quarters, replacing investment demand that often funnels into the one- and 2-bedroom types for OCR launches.

Singapore has a compact real estate landscape and developed information systems that property owners and buyers can quite easily access.

The private residential market here is therefore not as imperfect as in countries with a geographical spread that has ‘distance gaps’ between one township to another, and little information about recent real estate transactions.

While there can be instances where there are pricing anomalies, today, buyers and sellers should not be overly concerned about overpaying or underselling. It boils down to what the parties to a transaction really want for themselves.

Alan Cheong is executive director, Research & Consultancy, and George Tan is managing director, Livethere Residential at Savills Singapore

")