[SINGAPORE] Through the past decade’s evolving global economic landscape and the Covid pandemic, Singapore remained resilient and vibrant in the world of real estate investment, attracting interest not just locally but also across borders.

Will this change after US President Donald Trump’s “Liberation Day” tariffs, which have roiled global stock markets and triggered concerns of an international trade war and a worldwide recession?

To be clear, Singapore has the lowest direct tariff rate of 10 per cent, but its trade openness and small domestic market make it vulnerable to trade outcomes in its key trading partners, most of which are directly affected by much higher tariffs. In the short term, there will be more market volatility and uncertainties.

The silver lining is that the fiscally sound Singapore government is prepared to support households and businesses if the situation deteriorates, and the Monetary Authority of Singapore stands ready to ease its monetary policy.

Global interest rates are also likely to drop in such a situation, which should benefit real estate investment. Hence, we believe real estate investors with a long-term view should stay invested in Singapore.

Singapore is third top cross-border investment destination in Apac

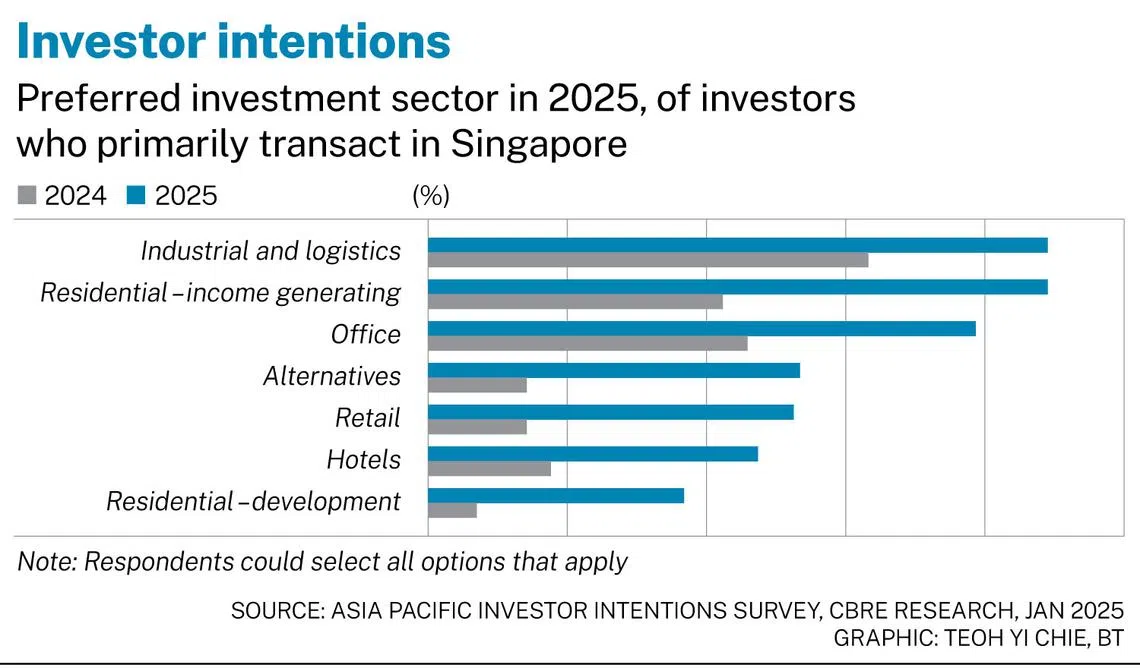

CBRE’s 2025 Asia Pacific Investor Intentions Survey found that, with further rate cuts forecast for this year, the majority of investors that transact in Singapore expect to purchase the same volume or more real estate over the course of 2025 compared with 2024.

A NEWSLETTER FOR YOU

Tuesday, 12 pm

Property Insights

Get an exclusive analysis of real estate and property news in Singapore and beyond.

Within the Asia-Pacific (Apac) region, the Republic ranked as the third most-attractive city for cross-border investment after Tokyo and Sydney, falling one place from 2024.

Thanks to Singapore’s macroeconomic stability, pro-business environment, and political-neutral stance, investors remain confident and interested in the country’s real estate assets for portfolio diversification and wealth preservation.

Amid the elevated interest rate environment, such investors will focus on core-plus to value-add strategies for higher yields.

Opportunities in industrial, living sector, office, retail and hotels

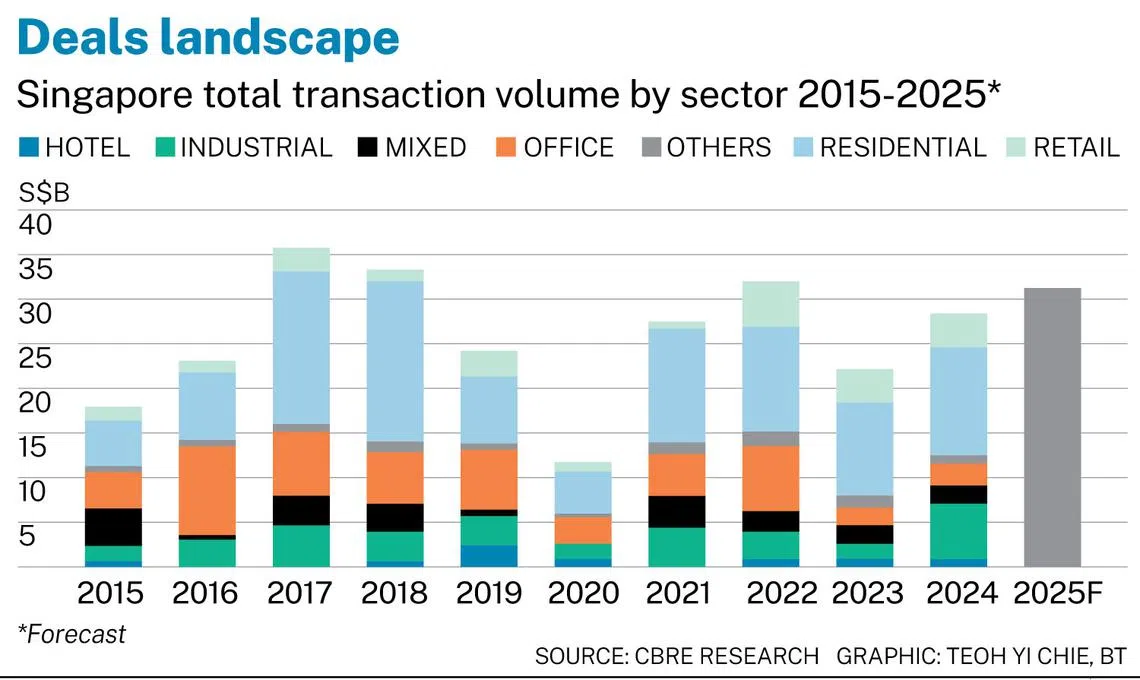

Real estate investment volumes rose 28 per cent year on year (yoy) to S$28.62 billion in 2024, rebounding from the 30.3 per cent yoy decline in 2023, which saw transactions tallying S$22.36 billion. Excluding public land sales, private transaction volumes were up more significantly by 35.9 per cent yoy, reversing the 45 per cent yoy decline in 2023.

Despite repricing pressures for most of 2024, capital values largely held firm, with prime logistics properties attracting strong investor interest as it was among the few sectors with a positive carry amid the elevated interest rate environment.

With fewer rate cuts and strong manufacturing momentum going into 2025, industrial and logistics assets retained their spot as the most preferred sector in 2025 in the Asia Pacific Investor Intentions Survey for Singapore-focused investors. The government’s innovative stance, incentives and initiatives towards growing and maintaining Singapore’s lead as an advanced manufacturing and logistics hub should signal a steady growth trajectory for industrial and logistics real estate.

After witnessing strong demand and rent growth of more than 50 per cent since Covid, the living sector has gained significantly more investor interest. In the survey, build-to-rent or income-generating residential assets have overtaken office properties as the second most-preferred sector in Singapore, reflecting a shift in the sector dynamics as well as the preferences of younger generations seeking community-driven environments.

The office sector could, nonetheless, see a rebound in investor confidence, after stronger return-to-office mandates and increasing demand for premium office space. Investments in assets that promote sustainability and well-being, such as green buildings, are also gaining traction. With Singapore’s Green Plan 2030 aiming to drive sustainability, properties that align with these goals could yield favourable returns.

Alternative sectors such as data centres and self-storage have also garnered investor interest. Meanwhile, appetite for retail and hotel assets remain resilient on expected tourism recovery and a robust calendar of concerts as well as meetings, incentives, conferences and exhibitions in 2025. Suburban retail space remains highly coveted due to its resilient demographic profile, population and income growth.

Supportive government policies

Nonetheless, ongoing headwinds may continue posing challenges to the market in the near term. Most survey respondents highlighted the uncertain geopolitical landscape, more-hawkish-than-expected central bank policy and escalating labour and construction costs as the top three challenges for the real estate investment market in 2025.

The government’s forward-thinking policies would thus be vital in this uncertain environment. Recent initiatives such as the extension and expansion of the Central Business District Incentive (CBDI) Scheme and the Strategic Development Incentive (SDI) Scheme should encourage both local and foreign investors to consider redevelopment options in the city centre.

Now, these CBDI and SDI schemes are not new. First launched in 2019, both schemes aim to encourage private owners to revitalise the city centre. The CBDI Scheme offers 25 to 30 per cent more gross floor area to spur owners of older, predominantly office buildings to redevelop their CBD properties into mixed-use projects to inject more homes and a live-in population. The SDI Scheme encourages owners of existing commercial buildings to team up with their neighbours to undertake a comprehensive redevelopment that would transform the street or precinct.

The schemes were well-received, despite the Covid disruption, with 14 of the 17 CBDI applications and seven out of 12 SDI applications having received in-principle approvals, several of which are already under construction.

On Feb 7, the Urban Redevelopment Authority announced that both schemes will be extended by another five years to 2030, and the CBDI Scheme’s scope widened to include the Cecil and Anson areas, allowing these to retain their existing commercial zoning as long as redevelopments here include at least 200 long-stay serviced apartments. An addition under the two updated schemes is the requirement of a sustainability statement, which will be reviewed by the authorities to assess the feasibility of retrofitting part of, or the entire existing building.

Earlier concerns of poor sales for residential projects in the CBD – due to hefty taxes on foreigners and investors buying residential properties – and subsequently the inability of developers to fulfil the Additional Buyer’s Stamp Duty clawback remission conditions, could now be alleviated with a majority commercial component and SA2 serviced apartment category or build-to-rent. It should give developers greater flexibility to meet market needs and introduce new living concepts, since there is still abundant rental demand in the CBD.

However, the introduction of new sustainability requirements could result in a sharp increase in costs and may deter some owners. We recommend that investors and owners partner up to combine expertise and diversify risks.

With a lack of CBD commercial development sites on the government land sales programme and a generally positive property outlook across major property segments, mixed-use redevelopments can offer investors significant opportunities in Singapore’s commercial real estate market.

Resilient state

Singapore’s real estate investment landscape stands resilient amid the uncertainties of the global economic environment. As one of the top three investment destinations in Apac, it offers multiple opportunities across multiple sectors, supported by favourable government policies.

With some regional markets experiencing property oversupply or structural adjustments, and some sectors, such as office and retail, becoming uninvestable, more investors are taking an interest in Singapore in view of its steady recovery and favourable supply environment.

The recent upheaval in the financial markets and potential recession in the US has presented more uncertainties globally. For retail investors, the volatility in the financial markets may either push them towards markets and asset classes that are more stable, such as the real estate sector in Singapore, or distract them as they await opportunities for value in the equities market. Their inclination in either of the above paths is likely to be influenced by the depth of market disruptions.

On a positive note, any recession in the US may quicken the pace of interest rate cuts by the Federal Reserve, which may consequently lead to sharper interest rate cuts across other markets.

In particular for institutional investors, the interest rate environment is likely to be more conducive for institutional grade asset transactions.

The path forward may be imbued with uncertainties, but the opportunities are vast for those willing to engage with this dynamic landscape.

Michael Tay is Singapore advisory deputy managing director and head of capital markets; and Tricia Song is head of research, Singapore and South-east Asia, at CBRE